Worldwide Rail Business: Lull Threatens New Business – Players Counting on Frowing After-Sales

Showing a growth rate of 2.3% in average over the upcoming five years, everything seems to be okay for the worldwide railway market at a first glance. However, in its eagerly expected study “Worldwide Market for Railway Industries” which is published every two years in the wake of the InnoTrans exhibition, SCI Verkehr shows significant differences, compared to recent years. While the market for new business clearly lost dynamics by showing an annual growth rate of only 1.3%, the After-Sales market will make up the lion’s share of worldwide revenues in the next five years, and will take the lead in terms of growth – a quiet transformation.

The turnover of the worldwide railway market is growing, however, more slowly than during the new building boom of the past two decades. While growth rates of 3-5% could be considered as a solid assumption then, the growth of today’s overall market by 169 billion Euro will mainly be driven by the increasing maintenance business until 2020. For the first time, more than half of the world wide turnover (53%) is made up by the After-Sales market. This is a consequence of intensive new building activities in recent years. “Many core products within the railway system have an operational life of 30 years or more. An initial investment in rolling stock or new tracks cause costs two or even three times higher than the actual asset price over its life-cycle. Especially suppliers and maintenance workshops are profiting from this” says Maria Leenen, CEO of SCI Verkehr. Restrained investment plans in China are hampering growth of the new building business in a special way, continues Leenen. “Furthermore, hopes for a higher demand in Russia and Brazil are unsubstantial – the roles of markets such as India, the Middle East or Turkey should be considered with critical scrutiny.”

Nevertheless, there are winners in the new building business: Comprehensive digitization of products and processes just reaches the railway systems. Since this facilitates substantial efficiency gains, SCI Verkehr expects notable momentum for rail operators and manufacturers: The railway industry will only be able to keep up in competition with other modes of transport with up-to-date process structures, optimized utilization of resources, and reduction of life-cycle-costs.

A detailed view on the markets

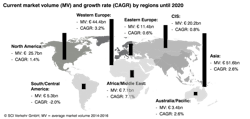

Asia – despite declined growth – keeps its status as biggest regional market with an overall volume of 51.6 billion Euro. Being still very small, the market of Africa/Middle East shows the highest dynamics with a 7.1% average annual growth rate.

Turnover of the Western European railway market is currently at 44.4 billion Euro. It has to be emphasized that – according to SCI Verkehr – the stable growth of 3.2% per year is mainly caused by higher investments in rolling stock and electrification projects.

Detailed analysis of all market segments and regions, the competitive landscape, and the manufacturers’ developments are provided in the study “Worldwide market for Railway Industries”, which is available since Wednesday this week.